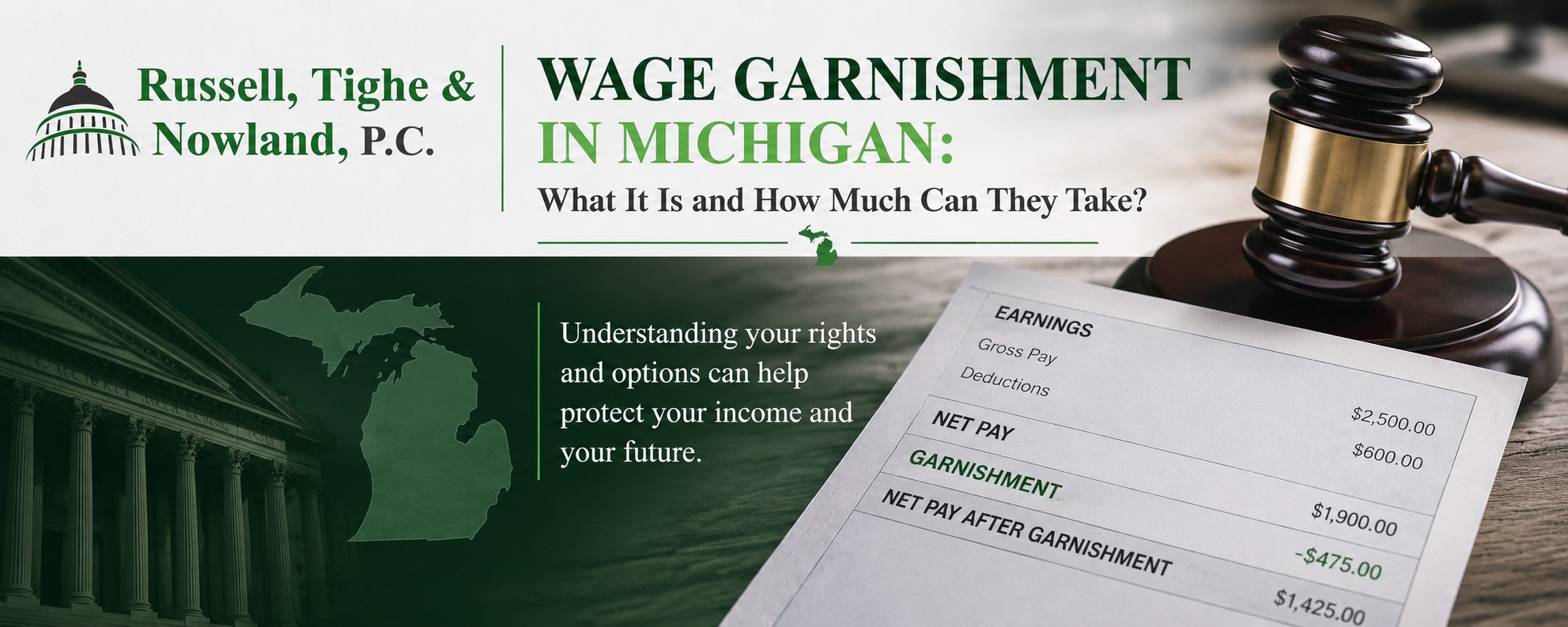

A wage garnishment can come as an unwelcome surprise for many Michigan residents. If you’ve fallen behind on credit cards, medical bills, personal loans, or other debts, a creditor may eventually obtain a court order allowing part of your paycheck to be taken before you receive it.

In Michigan, a wage garnishment is a legal process where an employer is required to withhold a portion of an employee’s earnings and send that money directly to a creditor to satisfy a debt. In most cases, the creditor must first sue you and obtain a judgment before garnishing your wages. However, certain debts, such as child support, taxes, and some federal student loans, may have different rules and may not require a traditional lawsuit.

So, how much can they take?

For most consumer debts, Michigan law generally limits wage garnishments to the lesser of:

- 25% of your disposable earnings, or

- The amount by which your disposable earnings exceed 30 times the federal minimum wage.

“Disposable earnings” means the amount left after legally required deductions, such as federal and state taxes and Social Security. Voluntary deductions for insurance or retirement plans are generally not subtracted when calculating disposable earnings.

Some types of debt have different garnishment limits. For example, child support obligations can result in garnishments of up to 50% or 60% of disposable earnings, depending on your circumstances. Federal tax debts and certain student loans also follow separate rules.

The good news is that receiving a wage garnishment does not necessarily mean you are out of options. Michigan law provides procedures for objecting to an improper garnishment, and some income may be exempt from collection. Additionally, filing for bankruptcy can often stop most wage garnishments immediately through the protection of the automatic stay. In some situations, bankruptcy may even allow you to recover wages that were garnished shortly before filing.

If your wages are being garnished, it is important to act quickly. The sooner you understand your rights and available options, the better your chances of protecting your income and regaining financial stability. An experienced Michigan bankruptcy attorney can review your situation and help determine the best path forward for you and your family.

Short answer, YES.

Medical debt is one of the leading reasons people in Michigan consider bankruptcy. A sudden illness, unexpected surgery, or ongoing medical treatment can quickly create overwhelming bills, even for individuals with health insurance. The good news is that, in many cases, bankruptcy can eliminate medical debt and provide a fresh financial start.

Medical bills are generally considered unsecured debt, meaning they are not backed by collateral like a home or vehicle. Because of this, they are often fully dischargeable in both Chapter 7 and Chapter 13 bankruptcy cases.

In a Chapter 7 bankruptcy, qualifying individuals may be able to eliminate most or all of their medical debt in just a few months. Once the bankruptcy court grants a discharge, creditors can no longer attempt to collect the discharged medical bills. This means no more collection calls, lawsuits, wage garnishments, or threatening letters related to those debts.

For individuals who do not qualify for Chapter 7, Chapter 13 bankruptcy can also provide significant relief. Chapter 13 allows debtors to reorganize their finances through a court-approved repayment plan lasting three to five years. In many cases, only a portion of the medical debt is repaid, with any remaining eligible balance discharged at the end of the plan.

One common misconception is that bankruptcy can only help if medical bills are the sole financial problem. In reality, bankruptcy addresses your entire financial picture. Credit card debt, personal loans, unpaid utility bills, and certain other unsecured debts can often be discharged alongside medical expenses. This comprehensive approach can make it easier to regain financial stability.

Filing bankruptcy may also stop pending lawsuits over unpaid medical bills. If a creditor has already sued you or is threatening wage garnishment, the automatic stay that goes into effect upon filing bankruptcy can halt most collection actions immediately.

It is important to understand that bankruptcy does not eliminate every type of debt. Certain obligations, such as most student loans, recent tax debts, child support, and alimony, generally remain payable. An experienced bankruptcy attorney can help determine which debts can be discharged in your specific situation.

If medical bills have become unmanageable, you do not have to face the burden alone. At Russell Law Firm, PC, we help Michigan families explore their options and determine whether bankruptcy is the right solution for their financial circumstances. A consultation can help you understand your rights and develop a plan to move toward a debt-free future.

Finding out that your paycheck is being garnished can be overwhelming. Losing a portion of your hard-earned wages can make it difficult to pay your mortgage, rent, utilities, and other everyday expenses. Fortunately, for many Michigan residents, filing for bankruptcy can provide immediate relief and stop wage garnishment.

How Does Wage Garnishment Work?

A wage garnishment occurs when a creditor obtains a court judgment against you and receives an order requiring your employer to withhold part of your paycheck to pay the debt. In Michigan, creditors may garnish a portion of your disposable earnings, subject to federal and state limits.

Common reasons for wage garnishment include:

- Credit card debt

- Medical bills

- Personal loans

- Deficiency balances after repossession

- Certain civil judgments

Some debts, such as child support, alimony, student loans, and certain taxes, have special garnishment rules.

Can Bankruptcy Stop a Garnishment?

In most cases, yes. The moment a bankruptcy case is filed, an automatic stay goes into effect. The automatic stay is a federal court order that generally prohibits creditors from continuing collection efforts, including wage garnishments.

If your wages are being garnished because of credit card debt, medical bills, or other unsecured debts, the garnishment usually stops as soon as your bankruptcy attorney files your case.

Your employer should receive notice of the bankruptcy filing, and the creditor must cease collection activities.

Chapter 7 vs. Chapter 13

Both Chapter 7 and Chapter 13 bankruptcy can stop wage garnishments.

In a Chapter 7 bankruptcy, many unsecured debts can be discharged entirely, eliminating the debt that caused the garnishment in the first place. Chapter 7 cases typically last about three to four months.

In a Chapter 13 bankruptcy, you enter into a court-approved repayment plan lasting three to five years. This option can help individuals who have regular income and need additional protection for assets or who have fallen behind on secured debts like a mortgage or car loan.

Timing Matters

If your wages are currently being garnished, waiting can be costly. Every paycheck that is garnished reduces your ability to catch up on other financial obligations. In some situations, money garnished shortly before a bankruptcy filing may even be recoverable, depending on the circumstances.

The sooner you speak with an experienced bankruptcy attorney, the more options may be available.

We Can Help

If you’re facing wage garnishment in Michigan, you do not have to handle it alone. Bankruptcy can often provide immediate relief and a fresh financial start. At Russell Law Firm, PC, we help individuals and families understand their options and develop a strategy to protect their income and financial future.

If your paycheck is being garnished or you’re worried that a garnishment may be coming, contact Russell Law Firm, PC, for a consultation to discuss whether bankruptcy may be the right solution for you.

If you are considering filing for bankruptcy, one of the most important steps is determining the value of your home. The value assigned to your property can affect whether your home is protected, the amount of equity you have, and the options available under both Chapter 7 and Chapter 13 bankruptcy. For bankruptcy purposes, your home’s value should reflect its fair market value—the price a willing buyer would reasonably pay for the property in its current condition at the time the bankruptcy case is filed.

Many homeowners mistakenly believe they should use the amount they paid for the house, the replacement cost listed on their insurance policy, or the local tax assessment. However, these figures may differ significantly from the property’s actual market value. Housing markets change over time, and factors such as neighborhood trends, property condition, and necessary repairs can all impact what a home is worth.

Accurately valuing your home is important because it helps determine your equity. Equity is calculated by subtracting the amount owed on mortgages and other valid liens from the home’s fair market value. The amount of equity you have may determine whether your property is protected by applicable bankruptcy exemptions. If your equity falls within the exemption limits allowed by law, your home may be shielded from creditors during the bankruptcy process.

Home valuation can also play a significant role when dealing with multiple mortgages. In some situations, particularly in Chapter 13 bankruptcy, a homeowner may be able to treat a second mortgage as unsecured if the home’s value is less than the balance owed on the first mortgage. Because these situations often involve legal disputes over property values, obtaining reliable evidence of the home’s worth is essential.

There are several methods available to estimate a home’s value for bankruptcy purposes. The most reliable option is a professional appraisal. A licensed appraiser will inspect the property, evaluate its condition, and compare it to similar homes recently sold in the area. Although an appraisal may involve additional expense, it provides strong evidence if questions arise during the bankruptcy case.

Another common option is a comparative market analysis, often prepared by a licensed real estate professional. This method examines recent sales of similar properties and provides an estimate of the home’s likely selling price. While generally less expensive than a formal appraisal, it can still offer valuable support for determining fair market value.

Online valuation tools can also provide a general estimate. Websites that analyze local market data and recent sales may offer a useful starting point for homeowners. However, these automated estimates cannot account for unique features or significant repair issues affecting a particular property. They should be viewed as informational rather than definitive.

Homeowners may also review recent sales in their neighborhood to estimate value. Comparing similar properties can provide a reasonable approximation, especially if professional valuation services are not immediately available. However, this approach may not be sufficient in more complex bankruptcy matters where precise valuation is necessary.

Determining the correct value of your home is a critical part of the bankruptcy process. An accurate valuation helps ensure that your bankruptcy schedules are complete, supports any exemption claims, and reduces the likelihood of disputes with the bankruptcy trustee or creditors. Working with an experienced bankruptcy attorney and, when appropriate, obtaining a professional appraisal can provide greater confidence that your home is properly valued and your interests are protected throughout the bankruptcy process.

If you’re considering filing for bankruptcy in Michigan, one of your main concerns is probably how long the process will take. The answer depends on several factors, including the type of bankruptcy you file, the complexity of your case, and how quickly you can provide the required information and documentation.

Chapter 7 Bankruptcy Timeline in Michigan

Chapter 7 bankruptcy is often referred to as a “fresh start” bankruptcy because it typically involves zero payments to your creditors, with your general unsecured debts being discharged. The process typically takes around three to six months in Michigan, but it can be longer if your case is complicated or if there are any objections from your creditors or the trustee that would result in additional hearings or involvement in negotiations.

Here is a general timeline of the Chapter 7 bankruptcy process in Michigan:

- Initial Consultation with Lawyer: We have a meet and greet where we go over your assets, debts, income and expenses to determine the best path for you.

- Pre-filing Credit Counseling: Before you can file for Chapter 7 bankruptcy, you must complete a credit counseling course from an approved agency. This typically takes one to two hours and can be done online or over the phone.

- Filing Bankruptcy Petition: You must file a bankruptcy petition with the court, along with various schedules and forms that detail your income, expenses, assets, and debts. These will be documents that we complete on your behalf, based on documents and information you you provide to us. After these documents are drafted, we will review these together for accuracy and completeness, and sign them before they are filed with the Court. Once filed, the automatic stay goes into effect, which stops most collection actions against you.

- Meeting of Creditors: About a month after you file your petition, you must attend a meeting of creditors, also called a 341 hearing. The trustee assigned to your case will preside over the meeting, and your creditors may attend to ask you questions about your finances. This meeting usually lasts about 10-15 minutes.

- Provide any Additional Documents (if requested): During the hearing the trustee may ask for additional documents. These are typical bank records, copies of checks, or proof of purchases or sales.

- Post-filing Counseling Course & Filing Fees: After you have provided everything the trustee needs, the last thing is to make sure you took your second course, and paid any outstanding filing fees to the court.

Chapter 13 Bankruptcy Timeline in Michigan

Chapter 13 bankruptcy is a reorganization bankruptcy that allows you to repay your debts over a period of three to five years. The process is more complex and takes longer than Chapter 7 bankruptcy, but it can be a good option if you have non-exempt assets you want to keep or if you’re behind on your mortgage or car payments.

Here is a general timeline of the Chapter 13 bankruptcy process in Michigan:

- Pre-filing Credit Counseling: Like with Chapter 7 bankruptcy, you must complete a credit counseling course before you can file for Chapter 13 bankruptcy.

- Filing Bankruptcy Petition: You must file a bankruptcy petition with the court, along with a repayment plan that details how you will repay your debts over three to five years. These will be documents that we complete on your behalf, based on documents and information you you provide to us. After these documents are drafted, we will review these together for accuracy and completeness, and sign them before they are filed with the Court. The automatic stay goes into effect when you file.

- Meeting of Creditors: About a month after you file your petition, you must attend a meeting of creditors, presided over by the trustee assigned to your case.

- Confirmation Hearing: About two to three months after you file your petition, you will attend a confirmation hearing, where the court will approve or deny your repayment plan.

- Repayment Plan and Discharge: If your repayment plan is approved, you must make payments to the trustee over three to five years. After you complete your payments, you should receive a discharge order from the court, which eliminates your dischargeable debts.

The length of a Michigan bankruptcy case depends on several factors, including the type of bankruptcy you file, the complexity of your case, and how quickly you can provide the required information and documentation.

Filing for bankruptcy can be a complex and stressful process, with many legal and financial considerations to keep in mind. One important issue to consider is the impact that filing for bankruptcy may have on your tax returns.

When you file for bankruptcy, it is important to make sure that all of your tax returns are up to date and filed with the appropriate government agencies. This is because bankruptcy courts require debtors to provide copies of their most recent tax returns to verify their income and expenses, and failure to provide these returns can result in your case being dismissed.

When you file for bankruptcy, it is important to make sure that all of your tax returns are up to date and filed with the appropriate government agencies. This is because bankruptcy courts require debtors to provide copies of their most recent tax returns to verify their income and expenses, and failure to provide these returns can result in your case being dismissed.

In addition, the timing of your bankruptcy filing can impact how your tax refunds are handled. If you file for bankruptcy before you filed your tax return, you may not know the exact value of your refund, leaving you unsure if you have enough in exemptions to protect your tax refund. This could result in part of your refund becoming part of your bankruptcy estate and subject to distribution to your creditors. However, if you file your bankruptcy after you receive your tax refund, you will make sure you keep accurate accounting of how you spent your refund.

It is also important to note that certain tax debts may be eligible for discharge in bankruptcy. Generally, income tax debts that are at least three years old and meet other specific criteria may be discharged in bankruptcy. So sometimes it might be worth holding off until after April 15th to file. However, it is important to consult with a bankruptcy attorney to determine your specific eligibility for discharging tax debts in bankruptcy.

If you are considering filing for bankruptcy and have outstanding tax debts, it is crucial to seek the guidance of an experienced bankruptcy attorney. Your attorney can help you understand how your tax returns and refunds will be impacted by your bankruptcy filing and can provide guidance on how to ensure that your bankruptcy case proceeds smoothly.

In summary, when filing for bankruptcy, it is important to ensure that all of your tax returns are up to date and filed with the appropriate government agencies. The timing of your bankruptcy filing can impact how your tax returns are handled, particularly in regard to any refunds that you may be owed. In addition, certain tax debts may be eligible for discharge in bankruptcy, and seeking the guidance of a bankruptcy attorney is essential to understanding how your tax returns and refunds will be impacted by the bankruptcy process.

For many of our clients, the annual tax refund they receive is a household necessity in order to pay for vehicle repairs, back rent, medical bills or child expenses. For that reason, we are often asked “will the court take my tax refund?”

Chapter 7

In a Chapter 7, you will be able to keep your tax refund as long as you have enough bankruptcy “wildcard” exemptions to do so. As of today (12/29/2022), the Wildcard Exemption is maxed at $13,100. Meaning, an individual may keep up to $13,100 of their tax refund, or a couple may keep $26,200 … so as long as you are not using your wild card exemption for other assets.

Chapter 13

Whether you are able to keep you tax refund in a Chapter 13 will come down to your budget. Annually you may submit a request to retain your tax refund, and with that you will need to show whether your income has gone up or down, as well as what unexpected expenses you had. So for example, if you want to retain your tax refund to pay your utility bills, the trustee may reject your request if your budget already accounting for those bills. However, if you need to retain your tax refund to replace the brake pads, rotors and calipers on your vehicle, there is a higher likelihood that would be approved.

Have additional questions? Please contact us using the form below.

The Exact Documents Vary Case To Case, But Generally Speaking These Are The Documents We Will Need:

- Pay Stubs For The Last 7 Months (Spouse Too, If Married)

- Tax Returns For The Last 2 Years (State & Federal)

- Bank Statements For The Last 90 Days.

- Recent Statements For Any Investment Accounts (401k, 403b, IRA, Pension, Stocks, Bonds, Etc.)

- Automobile, Motorcycle, Boat & Trailer Titles – If Applicable

- Automobile Lease – If Applicable

- Residential Lease – If Applicable

- Recorded Mortgage – If You Own Your Home

- Recorded Deed – If You Own Your Home

- Recent Property Tax Bill – If You Own Your Home

- Divorce Judgment (If Divorce Ordered Within The Past 8 Years)

- Child Support Orders – If Applicable

Have a question on what documents you need to file a Bankruptcy? Call us at 616-920-0555 or use the Contact Form below.

People often call in asking if their taxes can be forgiven in bankruptcy. And the answer is … maybe. Let’s dive in further.

In order to have your taxes forgiven, you must pass the 3/2/240 Rule:

3: Your taxes must have been due at least 3 years ago. So for example, your 2018 taxes are due April 15, 2019. That particular tax year passes the “3 rule” on April 16, 2022. Keep in mind here, if you filed an extension that year, making your taxes not due until October 17, 2019, then you would not pass the “3 rule” until October 18, 2022.

2: You must have filed your taxes 2 years prior to filing your bankruptcy. Now, YOU must have filed that return yourself. If the IRS filed a substitute return on your behalf, then you will not pass the “2 rule” per the bankruptcy code. In a situation where the IRS filed the tax return on your behalf, it’s not too late to then turn around and file your own return, and let the clock run.

240: The IRS must have assessed the income tax debt at least 240 days before you file your bankruptcy petition, or not at all. Assessed just means that the IRS is went through your tax return to make sure that everything is correct.

Also, your taxes will not ne discharged if:

- The taxes are income taxes. Taxes other than income, such as payroll taxes or fraud penalties, can never be eliminated in bankruptcy.

- You committed fraud or willful evasion. If you filed a fraudulent tax return or willfully attempted to evade paying taxes, such as using a false Social Security number on your tax return, bankruptcy can’t help.

- The IRS already placed a Federal Tax Lien on your property

Have a question on what tax debts can and cannot be forgiven in a Bankruptcy? Call us at 616-920-0555 or use the Contact Form below.

What debts can be forgiven in a bankruptcy? General Unsecured Creditors, and Secured Debts where you are surrendering the property.

General Unsecured Creditors: The most typical types of General Unsecured Debts that are forgiven are:

- Credit Cards

- Medical Bills

- Evictions

- Foreclosures

- Repossessions

- Some Taxes

- Payday Loans

- Personal Loans

Below are a list of unsecured debts that are not eligible for discharge:

- Student Loans

- Child Support

- Criminal Restitution

- Fines, Fees

- Some Taxes

Secured Debts where you are surrendering the property: So for example let’s say you have a secured home loan, but you owe more on it than it is worth. In a Bankruptcy you have the option to surrender that property, and have that debt be forgiven. This also goes for any vehicle loan, and any loan where there is a lien on a specific piece of property.

Now there is an exception to this rule. You cannot have any debt forgiven that was the result of fraud. The most typical example of this is when you lied on your credit application, or where you had no intentions to ever pay back a loan, or perform the service.

Have a question on what can and cannot be forgiven in a Bankruptcy? Call us at 616-920-0555 or use the Contact Form below.